Randle’s Ramblings #4

Liquidity and the Illusion of Stability - Ian Randle | September 2025

Liquidity and the Illusion of Stability

Liquidity is the oxygen of markets. It is invisible, often ignored, but utterly essential. When it is plentiful, markets look calm, resilient, and strong. When it disappears, panic sets in and the veneer of stability evaporates overnight.

We have lived through both extremes. The global financial crisis was liquidity drying up so completely that the pipes of the system froze. The COVID crisis was policymakers flooding those pipes with more liquidity than ever before. Today, as we sit in late 2025, the big question is simple: where is all this liquidity coming from, and how long can it last?

The answer is complicated. Liquidity is not just money printing, nor is it simply interest rates. It is a constellation of fiscal flows, central bank policy, private credit creation, shadow banking, and now even crypto rails. To understand the next wave of macro conditions, we need to dissect where liquidity is entering the system, where it is being withdrawn, and how those forces interact with the asset classes we care about.

The Mirage of Abundance

The market narrative today is one of resilience. US equities are near all-time highs. Bitcoin has weathered rate volatility and remains firmly in the six-figure range. Credit spreads are tight. VIX is subdued.

It all feels eerily stable. But is it?

Liquidity-driven rallies often lull investors into believing stability has been achieved, when in fact fragility is building beneath the surface. A dam looks strongest right before it bursts. And today, the cracks are not in the dam itself but in the fiscal foundations propping it up.

The Fiscal Engine

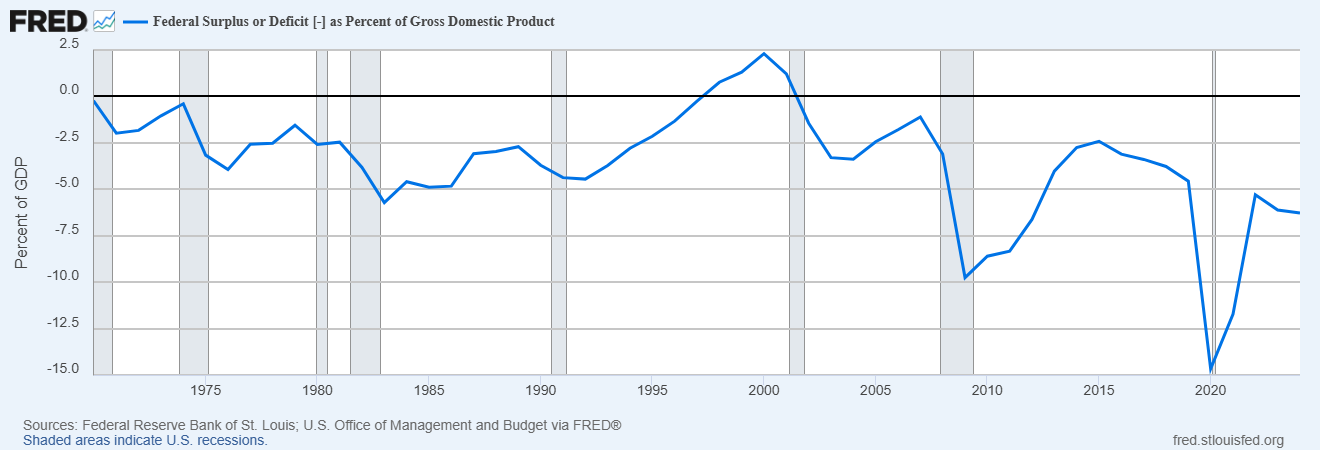

The single most important driver of liquidity in 2025 is not monetary policy, but fiscal policy. The US government is running persistent deficits north of 6% of GDP. Those deficits are financed through issuance, and when markets absorb that issuance without yields spiraling higher, the net effect is more cash sloshing through the system.

Deficits do not just fund government programs; they become the raw material for private balance sheets. Every Treasury issued is someone else’s asset. Every deficit dollar creates a corresponding surplus somewhere in the private sector. In other words, fiscal deficits are liquidity creation machines, even if the intention is not to juice markets.

But this engine is not perpetual. At some point, the cost of servicing debt (already above $1 trillion annually) creates political and economic constraints. That moment has not yet arrived, but the higher-for-longer rates regime ensures it will come sooner than many think.

The Monetary Counterbalance

While fiscal deficits have been a tailwind, monetary policy has been a counterweight. The Fed is shrinking its balance sheet through quantitative tightening (QT), pulling reserves out of the system. In past cycles, QT was enough to destabilize markets. This time, fiscal deficits are offsetting QT, creating a tug-of-war between monetary withdrawal and fiscal injection.

This is why asset prices remain buoyant despite restrictive policy rates. It is not that the Fed has lost control; it is that fiscal policy has overpowered monetary policy in providing liquidity. The market sees the oxygen flowing in and breathes easier, even as the Fed tries to tighten.

The Private Market Multiplier

Liquidity is also amplified by private credit creation. Shadow banking, structured credit, and private lending markets are booming. As banks pull back, private funds have stepped in, recycling institutional capital into leveraged credit exposure.

This is a multiplier. Every dollar of fiscal injection gets levered two or three times through private channels. That leverage is why markets feel more stable than they should. But it is also why a reversal would be more violent than expected.

The Crypto Layer

One of the most fascinating developments is that stablecoins have become part of global liquidity. At $180 billion and rising, stablecoins (using USDT as a representative example) are not yet systemically large, but they are systemically important. They provide an instantly liquid, dollar-denominated asset that can move at the speed of code, not at the speed of banking rails.

Stablecoin issuance is a liquidity injection. Redemptions are a liquidity withdrawal. This dynamic links the crypto economy to the broader dollar liquidity cycle. If capital flees risk assets, stablecoin redemptions tighten liquidity just as surely as Fed QT. If capital floods in, stablecoin supply expands and amplifies risk-taking.

The Illusion of Stability

Put these pieces together and you see the paradox. Markets look calm because liquidity is abundant. But the abundance is artificial, created by fiscal firehoses and private leverage. Stability today means fragility tomorrow.

This illusion is dangerous because it encourages investors to mistake liquidity for solvency. Rising asset prices hide balance sheet weakness. Tight spreads disguise credit risk. Low volatility conceals systemic fragility. When the tide turns, the unwind will not be orderly.

Historical Echoes

History offers plenty of warnings. The 1990s dot-com boom was liquidity-driven, fueled by Greenspan’s put and fiscal surpluses recycling into private speculation. The 2000s housing bubble was liquidity-driven, powered by securitization and shadow credit. The 2010s everything bubble was liquidity-driven, thanks to QE infinity.

Today is no different. We are in another liquidity-driven cycle, only bigger, because fiscal has joined monetary in supplying the fuel. The illusion of stability is stronger than ever, but the underlying risks are too.

Positioning for Reality

So how do investors navigate this?

First, by recognizing that liquidity cycles matter more than valuation in the short term. Expensive assets can get more expensive if liquidity is abundant. Cheap assets can stay cheap if liquidity is scarce. Fighting liquidity is fighting gravity.

Second, by acknowledging that liquidity is finite. Fiscal firehoses will eventually be constrained. Private credit cycles will eventually turn. Stablecoin flows will eventually reverse. Preparing for that moment is the essence of risk management.

Third, by using liquidity cycles as guides rather than absolutes. In 2025, the path of least resistance remains higher for risk assets, but the risks are compounding under the surface. The illusion of stability will hold, until it doesn’t.

A Note on Bitcoin

Bitcoin is the purest expression of liquidity sentiment. It thrives when liquidity expands and suffers when liquidity contracts. That is why Bitcoin is often the first mover in liquidity-driven rallies and the first casualty in liquidity withdrawals.

Where does that leave us today? The fiscal firehose suggests Bitcoin can grind higher into 2026, perhaps toward $180,000–200,000 if deficits persist and stablecoin supply keeps growing. But the illusion of stability also means that when liquidity reverses, Bitcoin will be hit hardest. Owning Bitcoin is owning a leveraged bet on liquidity.

Conclusion: The Oxygen of Markets

Liquidity is not everything, but it is close. It is the oxygen of the system. Right now, there is plenty of oxygen, which is why markets look calm. But investors must remember: too much oxygen also makes the system flammable.

The illusion of stability is powerful, but it is still an illusion. Wise investors will ride the liquidity wave while preparing for the moment when the tide turns. That preparation will determine who survives the next liquidity drought and who drowns in it.

Weekly Roundup

Macro: Cuts into Inflation

The Fed is cutting into sticky inflation, creating a dangerous feedback loop.

Services inflation at 3.6% remains elevated.

Wage growth still above pre-2019 levels.

Market pricing 50 bps of cuts this year, 80 bps next year.

This is not easing into weakness; it is easing into strength, raising long-term inflation risks.

Markets: Animal Spirits in Small Caps

Liquidity rotation is driving flows into small caps.

Russell 2000 outperformance vs. NASDAQ in recent months.

Buyback blackout creates headwinds for large-cap support.

Historical September seasonality (-0.7% average return) meets unusual liquidity strength.

Crypto & Blockchain: Stablecoins as Liquidity Rails

Stablecoins now process over $2 trillion annually in organic volume.

Integration with payment giants (Visa, Stripe, PayPal) shows mainstream adoption.

The next phase: tokenized deposits, bridging bank money with blockchain rails.

Crypto markets increasingly trade like liquidity futures, led by stablecoin issuance.

AI: The Datacenter Bubble

Global datacenter capex 2025 estimated at $400B.

Revenue far behind, margins compressed, risk of overbuild.

Historical parallels: Global Crossing (fiber in 2000), shale oil (2014).

AI is real and transformative, but capital cycles still apply.

Trading & Options: Positioning for Liquidity Cycles

In abundant liquidity, vol selling works… until it doesn’t.

SKEW index trending lower, complacency in options pricing.

Opportunities in structured call spreads on BTC and ETH.

Macro overlay: long volatility is cheap insurance against liquidity shock.

www.derive.xyz is the largest exchange for onchain options.

Recommendations this week

Book: The New Lombard Street by Perry Mehrling - on central banks as dealers of last resort. https://www.amazon.co.uk/New-Lombard-Street-Became-Dealer/dp/0691143986

Essay: Brent Johnson’s Dollar Milkshake Theory - explains liquidity flows and dollar dominance.

Podcast: Kyla Scanlon interview with Lynn Alden - 2 years ago but points still stand!

Cheers,

Ian

Ian Randle is a Core Contributor at Derive.xyz and Founder of SettledHere.com